Relazioni Trimestrali

Carmignac Emergents: Letter from the Fund Managers

-

-6.6%Relative performance of Carmignac Emergents A EUR Acc

versus its reference indicator MSCI Emerging Markets NR Index.

-

20.1%Of the current portfolio

is invested energy transition and renewable industries.

-

70.0%Exposure of Fund

to companies aligned with SDGs and sustainable themes.

Carmignac Emergents1 (A EUR ACC, ISIN FR0010149302) was down -11.53% in the first quarter of 2022, against a -4.92% decline in its reference indicator2. Emerging-market equities lost considerable ground in a quarter marked by the Russian army’s invasion of Ukraine. These equities underperformed those of the developed world, partly because of Russia’s weighting in the region but also because of a further -12.30% drop in the Chinese market (in EUR).

What happened in emerging markets in Q1 2022?

Before the invasion, we had 5.5% of the Fund’s assets invested in Russia. This Russian exposure was based on several factors. The country had excellent economic fundamentals, very low public-debt levels (less than 20% of GDP), and high foreign-currency reserves (over 43% of GDP) thanks to a large current-account surplus (nearly 10% of GDP) and a hefty fiscal budget surplus (some 4% of GDP). We had also identified high-quality companies in Russia with attractive valuations, good growth prospects, and excellent corporate governance. But when Putin recognised the independence of the separatist regions in Donbas, and we realised that war was about to break out, it was too late to sell our Russian stocks. Financial-market intermediaries had stopped trading Russian assets when the first sanctions were announced. We therefore decided to value our Russian holdings at close to zero and book a sizable loss, to reflect the fact that it had become impossible to close out our positions.

Another development that shook financial markets in the first quarter – and what explains most of our underperformance – was the sell-off in Chinese stocks (39% of the Fund’s assets at 31 March) following the outbreak of the war in Ukraine. Many investors, particularly in the US and UK, decided to offload their Chinese stocks when Putin and Xi reaffirmed their relationship through an official statement in late January. What’s more, the SEC began naming the first ten Chinese companies that will have to delist from US exchanges by 2024, underscoring US investors’ perception of China as an “uninvestible” market. We believe this fresh slump in Chinese equities is overblown and see it as a good opportunity to build up our exposure. The MSCI China Index has fallen back to levels last seen in 1993, when China’s GDP was 40 times smaller than it is today and the country was still eight years away from entering the World Trade Organization. Several companies in our portfolio have a market capitalisation that is below their cash level – something we haven’t seen since the 2008 financial crisis. Chinese stocks are trading at prices that seem to factor in a major break in diplomatic ties with the Western world, which could occur if Beijing gives military support to Putin, for example, or if China’s army invades Taiwan. We believe both of these events are highly unlikely at this point. Rather, we think China will maintain its neutral stance on the war in Ukraine and won’t take the risk of an escalation in Taiwan, especially since Western countries have shown they are united and determined in introducing heavy political sanctions.

Adjustments and current positioning

We took advantage of the excessive decline in Chinese stock prices to add two new companies to our portfolio. The first is Sungrow, listed locally in Shanghai. Sungrow is the world’s leading producer of electrical components for the solar power industry. It has a 25% share of the global market1 and is ideally positioned in a sector experiencing secular growth, fuelled further by the war in Ukraine and the EU’s plans to step up its investments in renewable energy and reduce its dependence on Russia. Sungrow also operates in the power-storage industry – another market with attractive growth prospects given the need for a steady power supply throughout the day. In addition, Sungrow has particularly effective waste, water and environmental-risk management policies, which include yearly targets for cutting CO2 emissions per unit of sales, and continuously improves its processes for waste treatment and recycling – all efforts which are tailored specifically to its operations. The second company is Beike, listed in the US. Beike used to be China’s biggest real-estate agency thanks to an expansive network of offices across the country. It then developed an online platform for housing transactions and grew into the world’s third-largest online sales plateform, behind Amazon and Alibaba2. Beike’s stock price fell sharply amid the broad downturn in China’s real estate market, to the point where we believe it’s trading at absurdly low levels given the quality of its management team. We sold our stake in China’s internet giant Baidu when the stock rebounded at quarter-end, booking a profit in the process, taking profit on the position.

Although the war in Ukraine forced us to lower our growth forecasts for 2022, we still think our Fund is well positioned for a significant rebound in the coming months. Our Chinese stocks could bounce back if Beijing comes to an agreement with US regulators on giving them access to the accounting data of Chinese companies. Meanwhile, our Korean stocks are also trading at depressed prices. That’s especially true for Samsung Electronics and LG Chem, even though these firms are global leaders in the fast-growing markets of semiconductor memory and EV batteries. Our holdings in Latin America (17% of the Fund’s assets) should keep doing well in light of higher commodities prices. Brazil (12% of the Fund’s assets)3 looks more attractive now that Lula, the leading presidential candidate, has formed an alliance with key centrist parties, diminishing the chances of a new government hostile to financial markets.

Carmignac Emergents is classified as an Article 9 fund under the Sustainable Finance Disclosure Regulation (SFDR)4, and was awarded France’s SRI certification in 2019 and Belgium’s Towards Sustainability label in 2020.5

As from 1st January 2022, Carmignac Emergents is classified as a financial product as described in Article 9 of Sustainable Finance Disclosure Regulation (“SFDR”). As such the Fund will invest mainly in shares of emerging companies that have a positive outcome on environment or society and derive the majority of their revenue from goods and services related to business activities which align positively with SDGs. This sustainable objective will be measured and monitored by the percentage of revenues aligned with UN Sustainable Development Goals (SDGs).

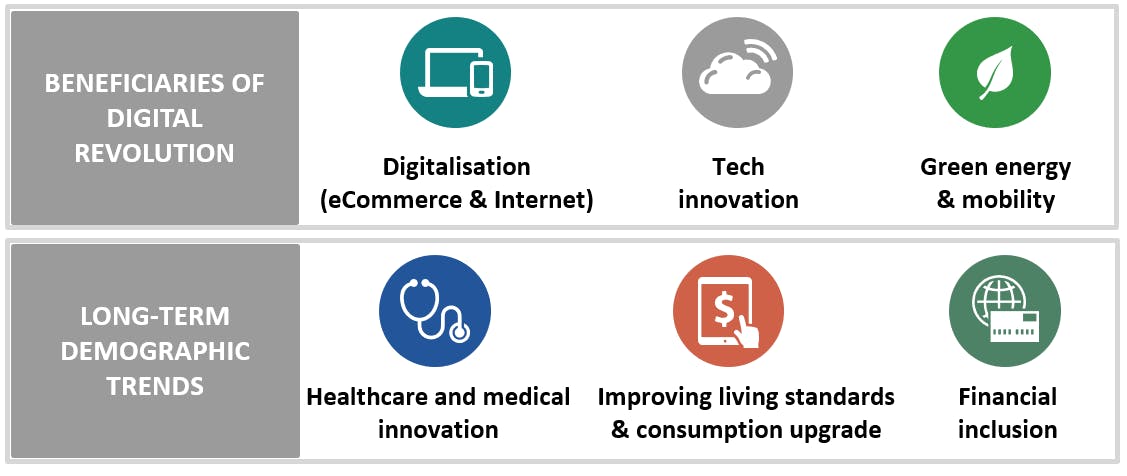

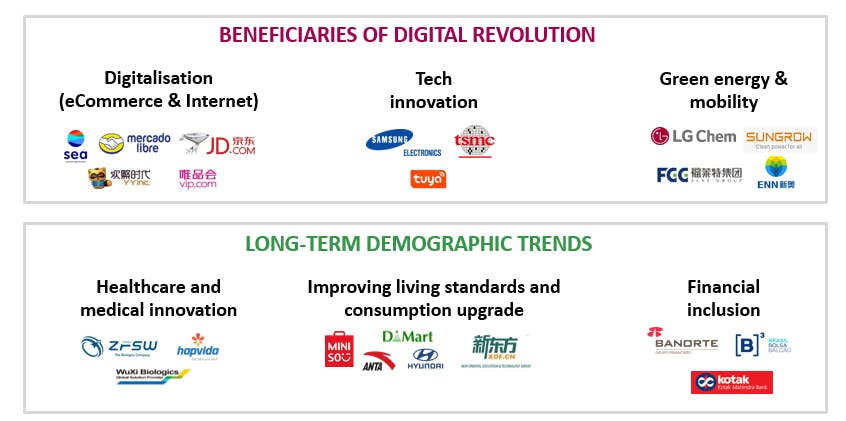

Our portfolio is currently structured around six major socially responsible investment (SRI) themes that are central to our processes.

As a reminder, our socially responsible approach is based on three pillars:

-

Invest selectively and with conviction

Giving priority to sustainable growth themes in underpenetrated sectors and countries with sound macroeconomic fundamentals.

-

Invest for positive impact

Favouring companies that deliver solutions to environmental and social challenges in emerging markets and reducing our carbon imprint by at least 30% relative to the MSCI Emerging Markets Index.

-

Invest sustainably

Consistently incorporating environmental, social and governance (ESG) criteria into our analyses and investment decisions.

Thematic allocation as of 31/03/2022: Focus on Beneficiaries of Digital Revolution & Long-Term Demographic Trends

Current Positioning as of 31/03/2022

Sources: Carmignac, Bloomberg, company data, EM Advisors Group, CICC, JPM Research, 31/03/2022.

1 Carmignac Emergents A EUR Acc Performance of the A EUR acc share class ISIN code: FR0010149302. Past performance is not necessarily indicative of future performance. The return may increase or decrease as a result of currency fluctuations. Performances are net of fees (excluding possible entrance fees charged by the distributor). From 01/01/2013 the equity index reference indicators are calculated net dividends reinvested. Performances in EUR as of 31/03/2022.

2 Reference indicator: MSCI EM NR USD) (Reinvested net dividends rebalanced quarterly).

3Source : Carmignac as of 31/03/2022, Brazil weight including Mercadolibre that realizes more than 50% of revenues in Brazil.

4The EU Sustainable Finance Disclosure Regulation (SFDR) 2019/2088 “lays down harmonised rules on the provision of sustainability-related information with respect to financial products”. For further information, see https://eur-lex.europa.eu/eli/reg/2019/2088/oj.

5Carmignac Emergents has been awarded the French and Belgian SRI labels. See https://www.lelabelisr.fr/en/ ; https://www.towardssustainability.be/ ; https://www.febelfin.be/fr.

Carmignac Emergents A EUR Acc

| 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 |

2024 (YTD) ? Year to date |

|

|---|---|---|---|---|---|---|---|---|---|---|---|

| Carmignac Emergents A EUR Acc | +5.76 % | +5.15 % | +1.39 % | +18.84 % | -18.60 % | +24.73 % | +44.66 % | -10.73 % | -15.63 % | +9.51 % | +5.26 % |

| Indice di riferimento | +11.38 % | -5.23 % | +14.51 % | +20.59 % | -10.27 % | +20.61 % | +8.54 % | +4.86 % | -14.85 % | +6.11 % | +4.42 % |

Scorri a destra per vedere la tabella completa

| 3 anni | 5 anni | 10 anni | |

|---|---|---|---|

| Carmignac Emergents A EUR Acc | -5.43 % | +6.93 % | +5.73 % |

| Indice di riferimento | -2.43 % | +2.96 % | +5.46 % |

Scorri a destra per vedere la tabella completa

Fonte: Carmignac al 28/03/2024

| Costi di ingresso : | 4,00% dell'importo pagato al momento della sottoscrizione dell'investimento. Questa è la cifra massima che può essere addebitata. Carmignac Gestion non applica alcuna commissione di sottoscrizione. La persona che vende il prodotto vi informerà del costo effettivo. |

| Costi di uscita : | Non addebitiamo una commissione di uscita per questo prodotto. |

| Commissioni di gestione e altri costi amministrativi o di esercizio : | 1,50% del valore dell'investimento all'anno. Si tratta di una stima basata sui costi effettivi dell'ultimo anno. |

| Commissioni di performance : | 20,00% max. della sovraperformance in caso di performance superiore a quella dell'indice di riferimento da inizio esercizio, a condizione che non si debba ancora recuperare la sottoperformance passata. L'importo effettivo varierà a seconda dell'andamento dell'investimento. La stima dei costi aggregati di cui sopra comprende la media degli ultimi 5 anni, o dalla creazione del prodotto se questo ha meno di 5 anni. |

| Costi di transazione : | 0,88% del valore dell'investimento all'anno. Si tratta di una stima dei costi sostenuti per l'acquisto e la vendita degli investimenti sottostanti per il prodotto. L'importo effettivo varierà a seconda dell'importo che viene acquistato e venduto. |

Carmignac Emergents A EUR Acc

Periodo minimo di investimento consigliato

Rischio minimo Rischio massimo

AZIONARIO: Le variazioni del prezzo delle azioni, la cui portata dipende da fattori economici esterni, dal volume dei titoli scambiati e dal livello di capitalizzazione delle società, possono incidere sulla performance del Fondo.

MERCATI EMERGENTI: Le condizioni di funzionamento e di controllo dei mercati "emergenti" possono divergere dagli standard prevalenti nelle grandi borse internazionali e avere implicazioni sulle quotazioni degli strumenti quotati nei quali il Fondo può investire.

CAMBIO: Il rischio di cambio è connesso all'esposizione, mediante investimenti diretti ovvero utilizzando strumenti finanziari derivati, a una valuta diversa da quella di valorizzazione del Fondo.

GESTIONE DISCREZIONALE: Le previsioni sull'andamento dei mercati finanziari formulate dalla società di gestione esercitano un impatto diretto sulla performance del Fondo, che dipende dai titoli selezionati

L'investimento nel Fondo potrebbe comportare un rischio di perdita di capitale.

Socially responsible investment still central to our approach

Since its inception in 1997, Carmignac Emergents has combined what we consider our emerging-market DNA since 1989 with our commitment to strengthening credentials in socially responsible investment. In welding together those two areas of expertise, we aim to add value for our investors while having positive impact on society and the environment.